Credit and Risk

Management

Advanced analytics that helps identify and mitigate risks

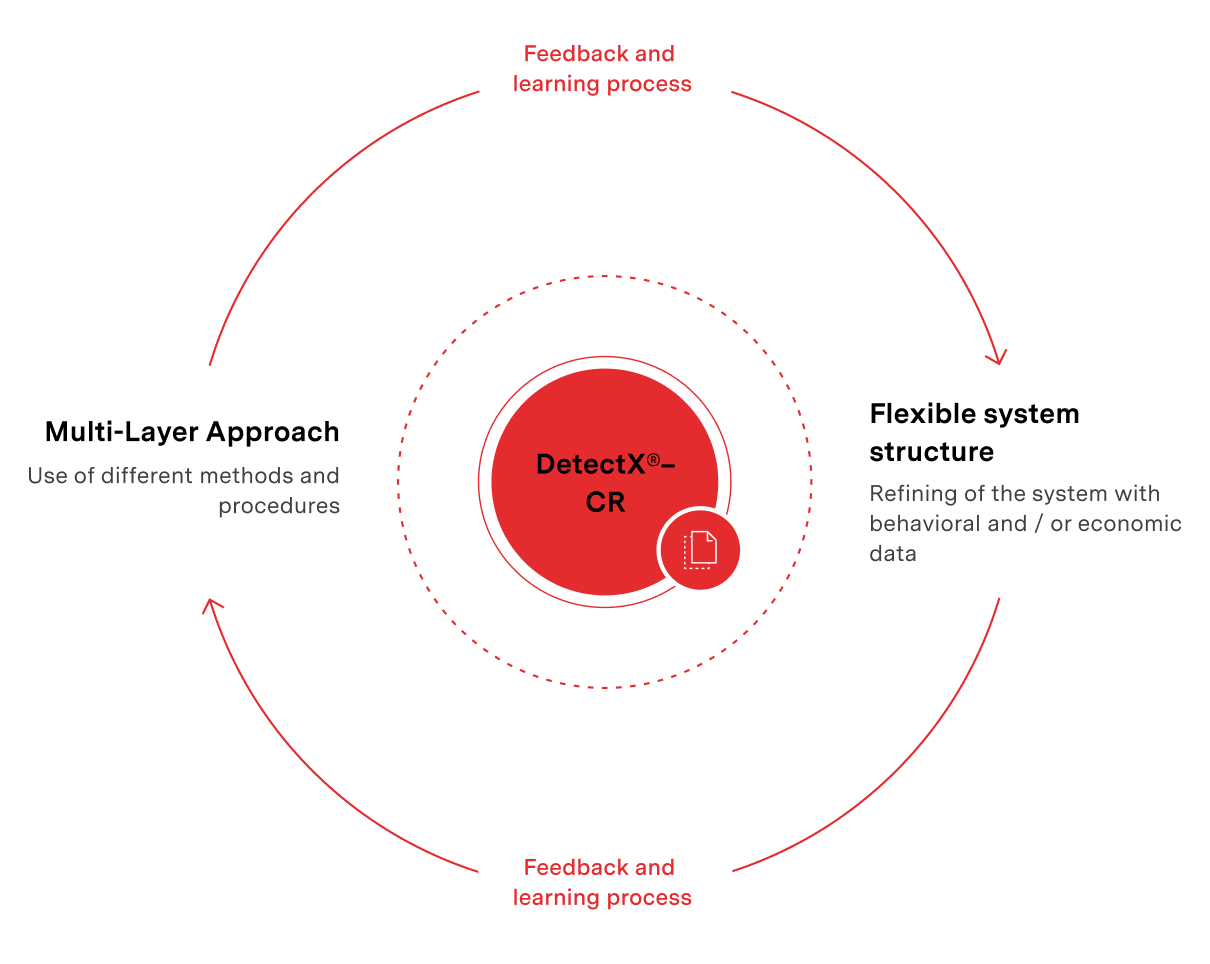

"State of the art" risk models are often based on statistical or stochastic approaches. Assumptions are made which are derived from theory, but which often can not handle fast changes in the real world. A dynamic solution, that includes real-time actions and continuously learns, combines theoretical approaches with practical experiences. DetectX® Predictive Analytics based risk models act in this way and adapt to dynamic changes.

Risk-based pricing in

Credit Risk Management

The use of modern rating systems to calculate risk-adjusted pricing is a key factor for success in the credit industry. These systems must be flexible and adaptive in their structure and in their ability to deliver consistent and reliable results.

Reliable data analytics with Prospero DetectX®

DetectX®-CR generates optimised rating models with minimised false alerts. These models are transparent in their structure and quality. The model qualities are presented with various indicators such as Gini index, True Positive Rates, False Positive Rates and AuRoc-Curve. The accuracy of the models continuously improves in the feedback learning process. All activities are recorded and are easy to understand.

A powerful

solution

DetectX®-CR includes functionalities that create new rating models, validate and calibrate existing models and analyse different risk strategies. DetectX®-CR also includes a specific module for stress testing.

Media Search

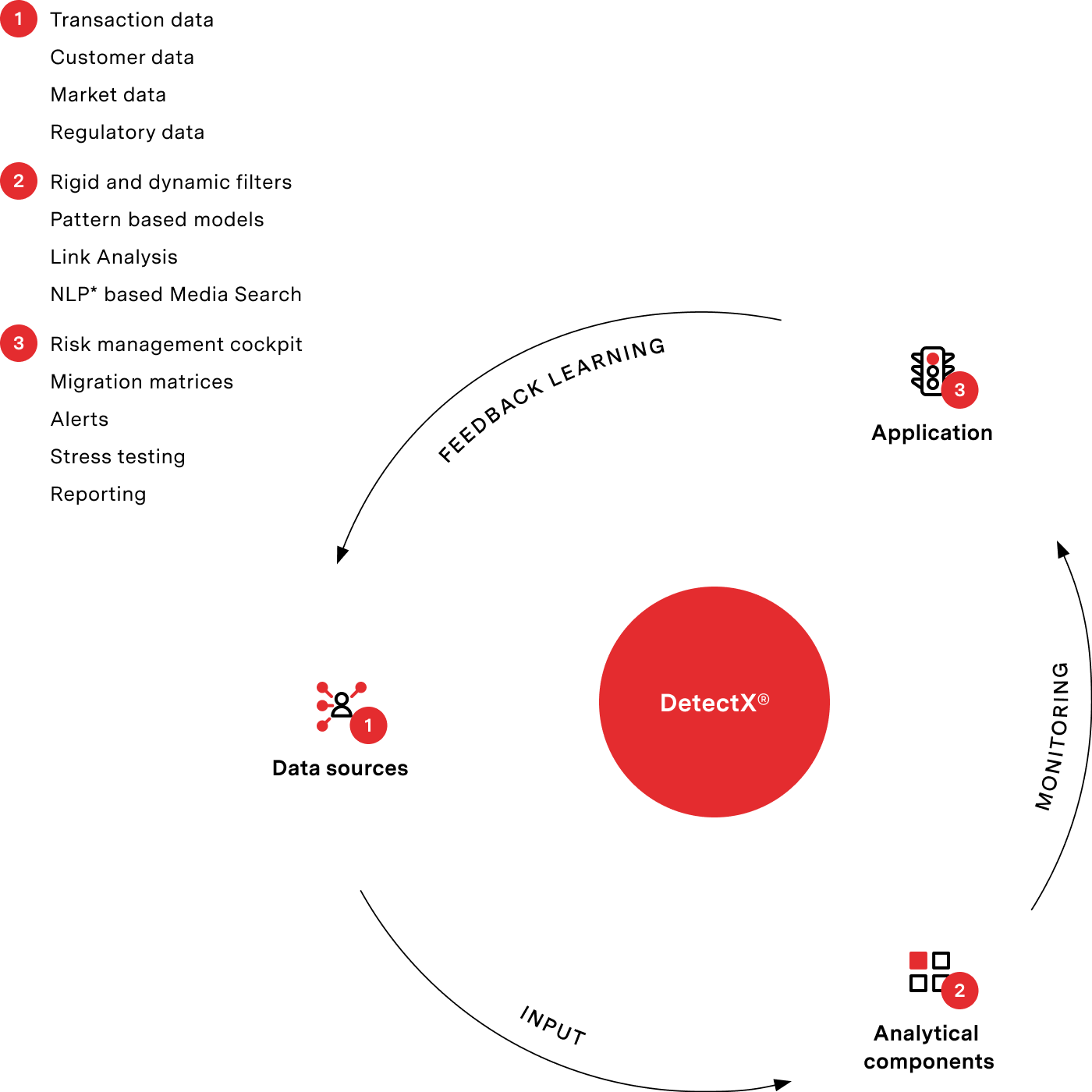

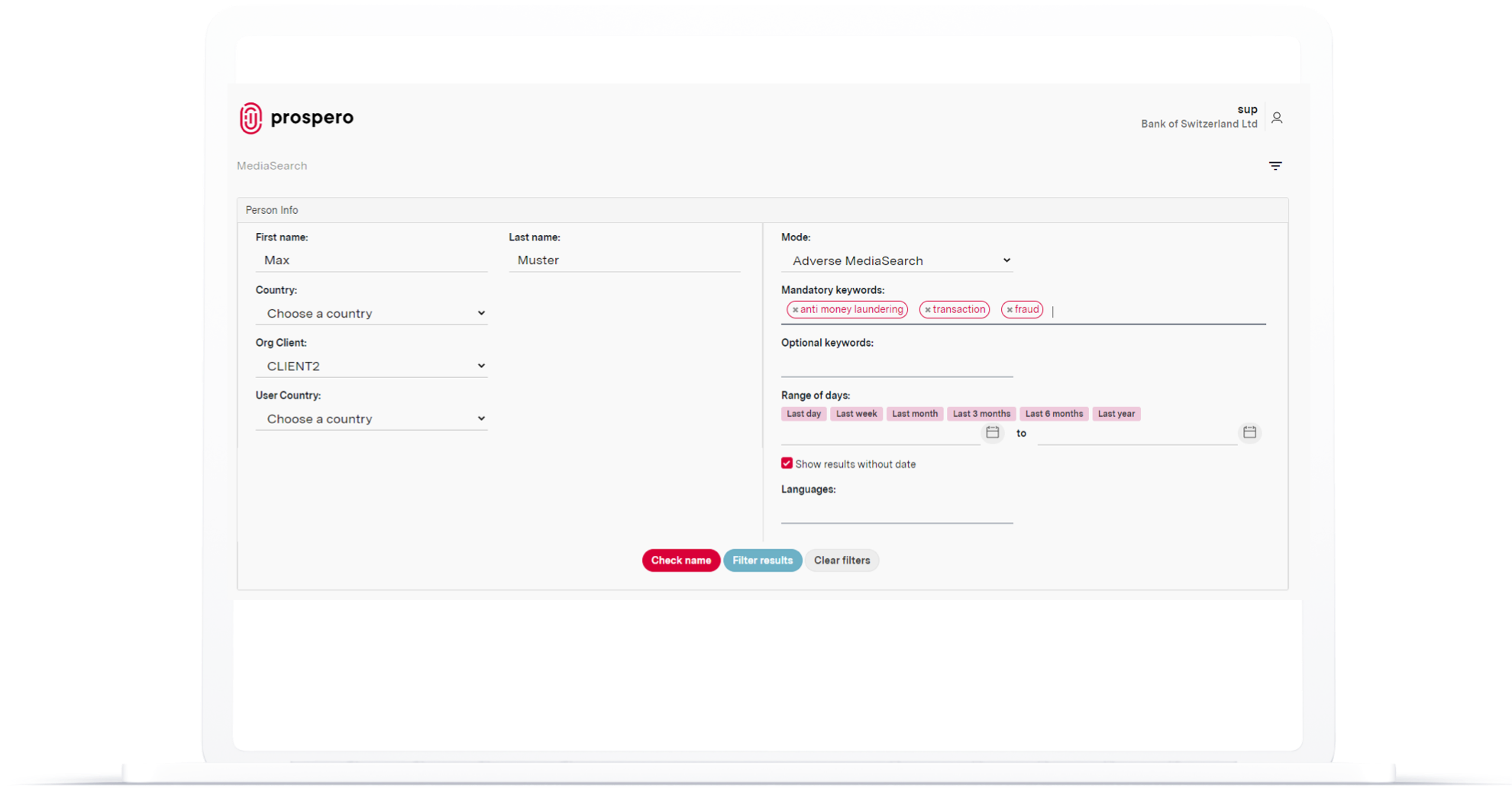

The MediaSearch module is used to find information on the Internet and in business information databases that is relevant to the valuation of a company (e.g. information on owners, legal disputes, product risks, etc.). These can be included in the rating and enables a holistic view of the company.

Macro and micro view

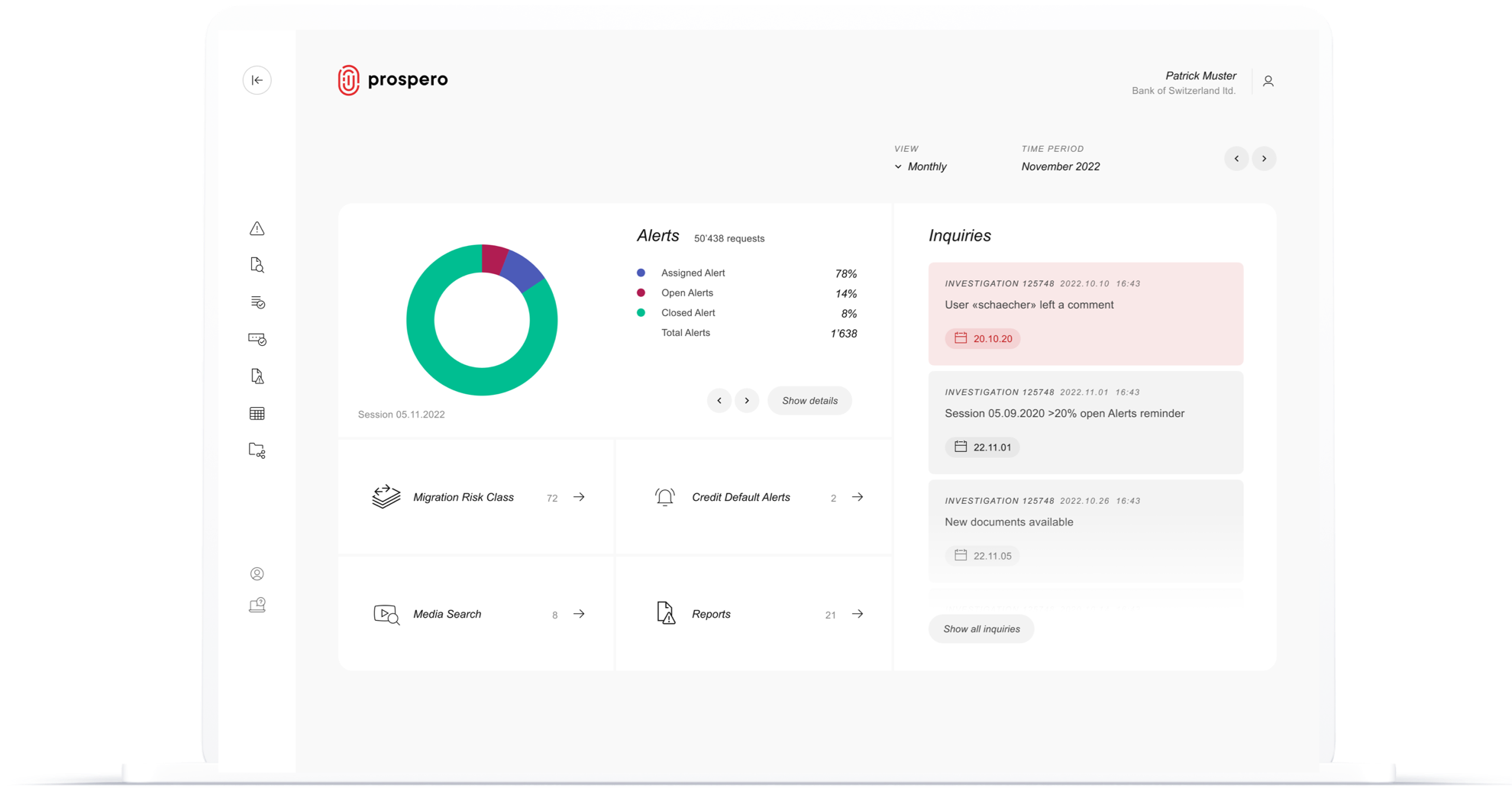

DetectX®-CR monitors credit portfolios using migration matrices with drilldown options to individual credit levels. Rating classes and classification models are flexibly defined.

DetectX®-CR is suitable for the creation, validation, calibration, benchmarking and stress testing of risk models in the finance industry. Examples beside credit risks include risk models for predicting claims risks in insurance or derivate risk models.

Key features of DetectX-CR

Compliance with the Basel II and III guidelines

Use for various rating models (corporate banking, retail etc.)

Calculation of PD (probability of default), LGD (loss given default) and EAD (exposure at default)

Analysis of individual credit and portfolio levels

Finding relevant information on the internet and in business information databases

Provision of a comprehensive assessment of a credit business, including early warning systems

General suitability for all areas where risk models are used

Benefits of DetectX-CR

Optimised rating and risk models

Transparency of financial implications of different risk strategies

Integrated stress testing

Comprehensive risk assessment

Regulatory requirements and compliance

In the area of Anti Money Laundering (AML), Fraud Detection and Prevention the products support the internationally recognised and accepted GAFI / FATF recommendations as well as the fulfilment of the regulatory requirements of the Swiss GwG, FINMA-GwV, VsB 16 and KAG on a very high-quality level.

The solutions are based on precise analytics and support the users in the fulfilment of the MiFID / EMIR requirements as well as the Swiss FinfraG, FidleG, BEHG, KAG and KKG acts, laws and regulations in the areas of risk based customer analysis, product suitability rule and exception handling, market transparency and cross border.

The products also support the qualitative and quantitative regulatory requirements in the areas of BASEL II/III, CRR and CRD IV minimal regulatory capital calculation, liquidity risk analysis (LCR / NSFR), static and dynamic stress testing and simulations, collateral optimisation and many others.

DetectX® Solutions

The DetectX® platform supports a range of powerful business solutions: